NRG ENERGY (NRG)·Q4 2025 Earnings Summary

NRG Energy Delivers Strong FY25, Extends 14%+ EPS Growth Through 2030

February 24, 2026 · by Fintool AI Agent

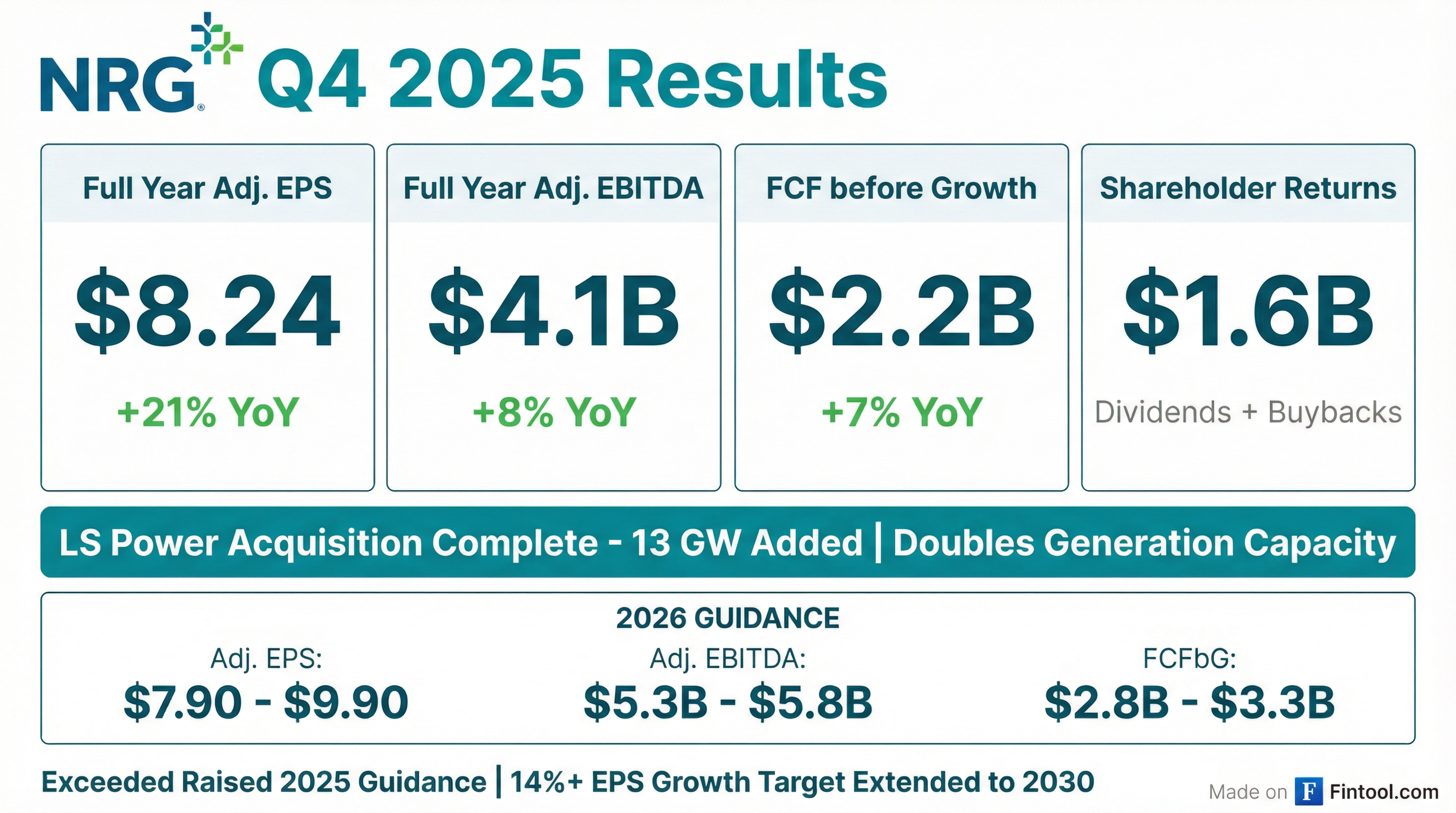

NRG Energy reported record full year 2025 results, delivering Adjusted EPS of $8.24 (+21% YoY) and Adjusted EBITDA of $4.1 billion (+8% YoY)—exceeding raised guidance ranges for the third consecutive year. The company extended its long-term growth outlook, now targeting 14%+ Adjusted EPS CAGR through 2030 (up from the prior 2029 target), with pro forma Adjusted EPS of $14+ by 2030. NRG also unveiled a significant data center opportunity representing >$2.5B in annual recurring EBITDA through 6 GW of long-term power agreements.

Did NRG Energy Beat Earnings?

Full Year 2025 delivered across the board. NRG exceeded its raised guidance ranges on all key metrics, marking a strong execution year ahead of the LS Power integration.

Q4 2025 was softer sequentially, with Adjusted EPS of $1.04 versus $1.56 in Q4 2024. The quarterly comparison is impacted by timing of realized hedge gains and mark-to-market effects. Management emphasized that the full year results—not individual quarters—reflect the underlying business performance given the volatility of unrealized derivative gains/losses.

GAAP Results: Net Income was $864 million ($4.43 EPS) for full year 2025, down from $1.1 billion in 2024. The decline was primarily driven by unrealized mark-to-market losses on economic hedges, which don't reflect expected economics at settlement.

Quarterly Progression (Adjusted EPS):

Q4 2025's $1.04 EPS was below Q4 2024's $1.56 primarily due to timing of unrealized hedge gains. Management emphasizes full-year results as the appropriate measure of performance.

What Did Management Guide for 2026?

NRG reaffirmed its 2026 guidance, which now incorporates approximately 11 months of contribution from the LS Power portfolio acquired on January 30, 2026.

Key guidance assumptions:

- ~90% of LS Power's estimated full-year 2026 contribution (11 months)

- Excludes fair value adjustments on derivatives

- Consistent with 14%+ Adjusted EPS CAGR target extended through 2030

The EBITDA guidance midpoint of $5.575B is 38% above prior consensus, reflecting the transformative impact of the LS Power acquisition. The company expects to provide additional long-term outlook detail on the earnings call.

What Changed This Quarter?

LS Power Acquisition Complete

The headline development: NRG doubled its generation footprint. On January 30, 2026, NRG closed on the $5.3 billion acquisition of 18 natural gas and dual-fuel facilities totaling 13 GW across nine states, plus CPower's commercial and industrial demand response platform.

The deal was funded by:

- $4.9 billion in new secured and unsecured notes issued October 2025

- Existing cash resources

Strategic rationale:

- Doubles NRG's generation capacity to ~25 GW

- Expands geographic footprint beyond Texas

- Adds CPower's demand response capabilities for C&I customers

- Positions company for "power demand supercycle" driven by data center growth

Texas Energy Fund Progress

NRG secured $1.15 billion in low-interest (3%) financing from the Texas Public Utility Commission for three generation projects totaling 1.5 GW:

All three projects are on time and on budget.

Winter Storm Fern Performance

NRG's Texas fleet demonstrated strong reliability during Winter Storm Fern in early 2026, achieving 97% in-the-money availability. Management noted: "Our assets were ready when the grid needed them. That performance reflects investments we have made in the plants in recent years and great work by our amazing people."

Virtual Power Plant Exceeds Targets

NRG's Texas Residential VPP program exceeded its raised 2025 target—finishing the year at nearly 10x the original objective. The company remains on track for:

- 1 GW residential VPP in Texas by 2035

- Expansion into PJM/East markets launching early Q2 2026

Battery Storage Contracts

NRG announced a series of contracts totaling over 1 GW of battery storage in Texas expected to come online by the end of 2026. The batteries will be used to serve retail customers and shift renewable power between hours as customer demand changes.

Data Center Growth Opportunity: >$2.5B Annual EBITDA

NRG unveiled its most detailed data center strategy yet, targeting >$2.5B in annual recurring Adjusted EBITDA from 6 GW of power agreements under 15-20 year terms.

2025 Progress:

- 445 MW of long-term (10-year, extendable to 20-year) data center load contracted

- 2026 target: At least 1 GW of contracted data center opportunities supporting "Bring Your Own Power" (BYOP) solutions

5.4 GW GEV/Kiewit Venture

NRG announced a Project Development Agreement with GE Vernova and Kiewit-TIC to develop 5.4 GW of new natural gas generation capacity:

Key advantages:

- All turbine capacity secured under equipment agreements with GE Vernova

- Kiewit-TIC is the most experienced EPC contractor for GE H-class projects

- Multiple GW of key electrical equipment already secured

- Several hundred MW of bridge power available beginning 2028 to support early customer load

Bridge Power Details: Management clarified that the most successful bridge power technology is "over-engineered reciprocating engines"—spinning steel that provides reliability. Bridge power allows hyperscalers to scale capacity while CCGTs are being built. Some hyperscaler customers want it, others prefer absorbing CCGTs directly into their portfolio.

Additionally, the LS Power portfolio adds ~1 GW of uprate opportunities in PJM through CT-to-CCGT conversions and traditional uprates.

How Did Segments Perform?

Full year 2025 Adjusted EBITDA by segment:

Texas (+19% YoY) was the standout, benefiting from improved wholesale margins and supply cost optimization, partially offset by higher planned maintenance.

Vivint Smart Home (+8% YoY) delivered record new customer additions and strong retention:

How Much Did NRG Return to Shareholders?

NRG returned $1.6 billion to shareholders in 2025 and outlined an expanded $18.3B capital allocation plan through 2030:

Key 2026 capital allocation items:

- Quarterly dividend of $0.475/share ($1.90 annualized), an 8% YoY increase—7th consecutive annual increase

- ~$960M in debt payments plus $70M in fees

- $620M capex for Texas new builds (offset by $650M TEF/incremental debt)

The long-term capital allocation represents a 55% increase from the prior 2026-2029 plan of $14.4B.

What's the Balance Sheet Position?

NRG ended 2025 with significant liquidity following the LS Power deal financing:

Total debt increased to $16.4 billion from $9.8 billion, reflecting the $4.9 billion note issuance and refinancing activity.

How Did the Stock React?

NRG shares closed at $176.52 on February 24, 2026 (earnings day), down 1.5% after hitting a new 52-week high of $182.04 intraday. After-hours trading showed shares recovering to $180.30.

Valuation context:

- 52-week range: $79.57 - $182.04

- Stock up ~122% from 52-week low

- Market cap: ~$33.8 billion

- 2026E P/E: ~19.8x (at $8.90 midpoint EPS)

- 2030E P/E: ~12.6x (at $14.00 pro forma EPS target)

The market appears to be pricing in confidence around the LS Power integration and NRG's positioning for the data center/AI power demand cycle. The 14%+ EPS CAGR extension and explicit data center EBITDA target provide clearer visibility into the multi-year growth runway.

What's the Upside from Power Prices?

NRG provided detailed sensitivity analysis showing significant upside from rising power prices—an important consideration given the data center-driven demand outlook.

2026 Base Assumptions:

- Texas ATC power price: $52/MWh

- PJM ATC power price: $53/MWh

- Henry Hub gas: $3.75/MMBtu

Illustrative Gross Margin Upside (Generation-Only, Fully Open):

Management noted that "forward curves do not reflect demand outlook"—suggesting current market pricing may undervalue the power demand supercycle thesis.

Excluded from base guidance (upside opportunities):

- Leverage to rising power and capacity prices

- Data center/large load premium PPAs

- 5.4 GW GEV/Kiewit venture contribution

- 1 GW PJM uprates from LS Power portfolio

What Should Investors Watch?

Near-term catalysts:

- LS Power integration execution — First full quarter contribution in Q1 2026

- T.H. Wharton COD — First TEF project expected online June 2026

- Data center contracts — Target at least 1 GW of BYOP opportunities in 2026

- Texas residential VPP expansion — Execute toward 1 GW by 2035 target

Key risks:

- Natural gas and power price volatility

- Integration challenges with LS Power portfolio

- Texas regulatory environment

- Customer affordability concerns constraining pricing

Q&A Highlights

The earnings call Q&A provided key details on NRG's data center strategy, contract structure, and near-term execution:

Data Center Contract Structure:

- Contracts structured as "very heavy capacity payment" plus a variable component that "turns into basically a heat rate for the hyperscaler—they take the gas risk"

- Pricing for 1.2 GW GEV turbine deals expected "north of the $90-$95 range"—on the high end to pay for equipment and returns

- Land transactions priced separately from the $95/MWh energy pricing

- Targeting "blocks in excess of a gig" with contracts of "minimum 10 and frequently 20 years"

Counterparty Standards:

- Exclusively targeting Tier 1 hyperscalers—"even inside of the universe of hyperscalers" based on credit quality

- Investment-grade counterparties required to support credit needs for 20-year contracts

Timing & Execution:

- First power from data center contracts could be online by "late 2029, then ratably probably one gig a year" after that

- 2026 target of 1 GW+ contracted is NOT included in guidance—represents pure upside

- PJM focus: Initially prioritizing the 1 GW of uprates over new build—"faster and quicker to market"

Financing Approach:

- Expects to use corporate balance sheet financing vs. project financing for data center projects

- Capitalization consistent with 3x leverage target at the corporate level

VPP Expansion:

- "Launching a VPP-like program in the East here early second quarter"

- Pacing well against the 300 MW target for 2027

- GoodLeap and Sunrun relationships supporting battery scale-up

ERCOT Batching:

- Company views ERCOT's batching proposal as "a great step forward to accelerate the process" for data center interconnections vs. serial approach

$2.5B EBITDA Opportunity Breakdown:

- The $2.5B annual EBITDA target corresponds directly to 5.4 GW new build plus 1 GW of PJM uprates—roughly 6 GW total

Organic Growth Composition:

- 14%+ CAGR breakdown: approximately 80% from organic growth, 20% from share repurchases

CEO Transition: Larry Coben announced he is approaching the conclusion of his time as CEO, though he will continue as an advisor and long-term shareholder. He noted: "Over the past 27 months, the NRG team has reshaped the portfolio, strengthened the balance sheet, and positioned NRG to compete and keep winning in a changing power market."

Key Management Themes

Affordability Through BYOP: NRG's "Bring Your Own Power" strategy requires large loads to fund the capacity they require, protecting existing ratepayers while enabling data center growth. The strategy centers on three pillars:

- BYOP for large loads — Data centers fund dedicated capacity through premium PPAs

- Smart energy savings — 1 GW residential VPP and C&I demand response reduce peak demand

- Grid reliability investments — 1.5 GW Texas Energy Fund projects add firm capacity for system stability

Record Execution: 2025 marked NRG's third consecutive year of raising and exceeding guidance, with top-decile safety performance. The company delivered $120M toward its $750M organic growth plan in 2025.

2026 Management Priorities

Management outlined six key priorities for 2026:

- Deliver financial, operational, safety, and business objectives

- Integrate LS Power portfolio — Complete construction of T.H. Wharton by June 2026

- Execute organic growth — Deliver 2026 contribution in line with $750M (2025-2029) plan

- Contract data center opportunities — At least 1 GW supporting BYOP solutions

- Expand VPP — Execute toward 1 GW Texas residential VPP by 2035

- Return $1.4B to shareholders — Grow dividend 7-9% (8th consecutive increase)

Related: